A guide to payment methods in international trade

Whether you are importing goods from abroad or selling to international buyers, the question of payment is an important one that must be answered early. However, due to the often-complicated nature of international trade, payment in these circumstances is not often straightforward.

There are several complex processes involved, and plenty of options to consider for how these payments can be made – usually called payment terms or methods of payment. Add the fact that the payment terms you pick can be a factor in determining how attractive your offer is, and things get even more unpredictable.

What are the types of payment methods you should know, and how do they compare with one another? This guide takes a deep dive into payment terms in international trade, including their meaning, how they work, and how to decide what’s best for you.

Table of Contents

Payment terms in international trade

When it comes to international trade, the process of buying and selling can be prolonged, and often complicated. So, it’s understandable to feel relieved after concluding a sale with the other party and agreeing on a price. But agreeing on a price is only one part of the payment process. You still need to agree on how payment will be made, and when. This is where payment terms come in.

Payment terms are the conditions that parties in international trade agree on to complete payment. They are often referred to as the methods of payment that exporters and importers can utilize to finalize their trade deal. Payment terms deal with many important issues relating to the trade deal. These include whether payment will be made before delivery, who retains ownership of the goods before delivery, and how payment will be made1.

Obviously, payment is an important part of getting a profitable trade whether you’re exporting or importing goods. But the payment terms that are utilized can play an even more important role in attracting good trades in the first place, especially for sellers. Buyers ideally want to delay payment as much as possible, preferably until they receive or even sell the goods. Sellers also want to collect payment as early as possible, ideally before they send the goods or immediately upon receipt. All of this makes finding the right payment terms a balancing act that both parties want to get just right.

With that said, let us move next to the types of payment terms in international trade and how they work.

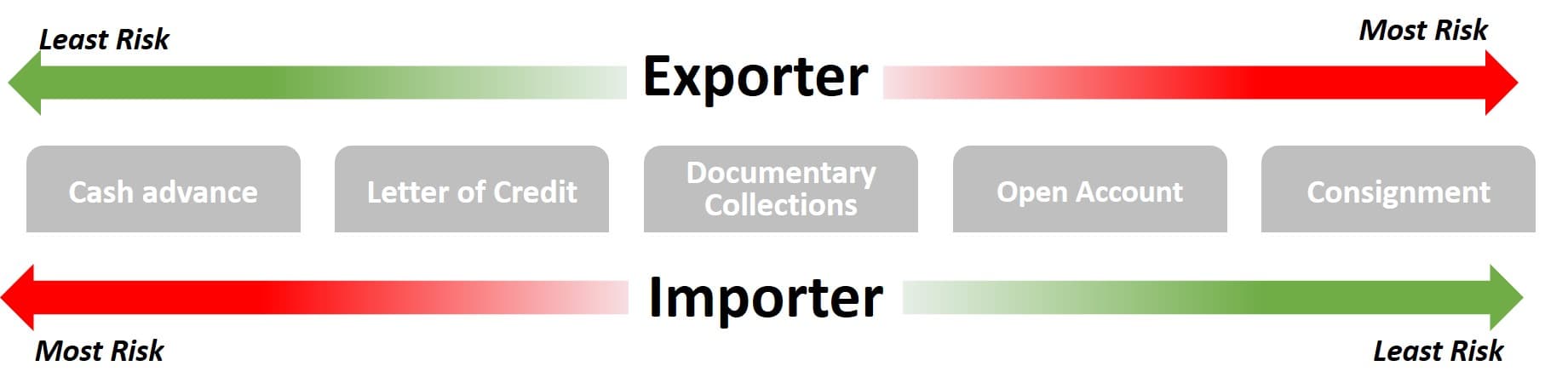

5 types of payment methods and terms

There are five major payment methods you will often see parties adopting in international trade. These are cash in advance, letter of credit, documentary collections, open account, and consignment. We will discuss each of these below.

1. Cash in advance

Also called ‘advance payment’ or ‘cash with order’, cash in advance means exactly what it sounds like. It is a mostly straightforward payment method where the importer (usually the buyer) pays for the goods upfront and before shipment. The payment may be completed by any means agreed between the exporter and the importer. Popular options include wire transfer, international cheque, and payment by debit card.

This payment term clearly favors the exporter because it means they receive payment while still in possession of the goods. A typical procedure for parties using this method is to agree that a set percentage of the price will be paid before production starts. After production, either all or most of the outstanding price will be paid before shipment. They may then agree that any amounts left will be paid upon receipt of the goods by the importer.

Cash in advance presents a lot of risk for the importer. This is because it puts them in a position where the exporter still has ownership and possession of the goods and has already received payment for the goods. It also creates an unfavorable cash flow situation for the importer because they have to pay all of the price upfronts and in cash – a position most buyers try to avoid.

Obviously, this payment option will only be available in rare situations. This can include where the order size is very small, or situations where the exporter is in a very strong negotiating position (such as where the goods are scarce). It can also be an option for exporters who are not convinced of the importer’s credit-worthiness, or where the importer completely trusts the seller.

As a result, exporters will very rarely offer this payment term because it presents so much risk for the buyer. If you want to attract more sales or a higher caliber of buyers, you will need to be more flexible with your payment terms, except where the special circumstances mentioned above exist.

2. Letter of credit (L/C)

Letter of credit is one of the most well-known terms of payment in international trade. It is also one of the most secure payment methods available2. This payment method is quite popular in the Middle East and China. It involves a payment process that is conducted by a bank on behalf of the importer. The letter of credit is a document that operates as a guarantee by the bank saying it will pay the exporter for the goods once certain terms and conditions are fulfilled. These terms and conditions are typically included in the letter of credit itself, and mostly have to do with inspecting the documents accompanying the goods, rather than the goods themselves.

Before an importer can obtain a letter of credit, they must be able to satisfy their bank of their credit-worthiness. When the bank completes the payment on behalf of the importer, they will turn towards the importer for reimbursement. This is usually based on terms agreed between the importer and the bank.

Letters of credit are mostly applicable in situations where the exporter and importer have a new and untested trade relationship. They can also be a good option where the exporter is not satisfied with the credit-worthiness of the importer or is unable to confirm this. Either way, a letter of credit provides less risk for the exporter since they have a solid guarantee of payment.

This payment term has its disadvantages though. For one, it is generally considered to be very expensive, as the banks involved will typically charge significant fees. The fees will vary depending on the importer’s credit rating and the complexity of the transaction. Also, the bank does not generally inspect the goods shipped by the exporter. This means there may be no provision to establish the quality of the goods in the process.

3. Documentary collections (D/C)

Documentary collection is a very balanced payment term that provides almost equal risk exposure for exporter and importer. This method is completed exclusively between banks acting on behalf of both parties. The process starts when the exporter ships the goods and sends documents needed to claim the goods to the importer. These documents usually include the Bill of Lading.

The importer also lodges payment with their bank with the instruction that payment should be made upon confirmation of the documents. Once the documents are confirmed, the documents will be released to the importer, enabling him to claim the documents. In this way, documentary collections work almost like escrow (which lets you lodge payment with a third party pending the completion of the agreement)3.

There are two major methods within this payment term. They are documents against payment (DAP) and documents against acceptance (DA).

- Documents against payment (DAP): Here, the agreement is that the bank will release payment to the exporter upon sighting the documents. No delay in payment is expected here, and once the documents are shown (and found regular), payment must be completed.

- Documents against acceptance (DA): Here, the agreement is that the documents will be delivered to the importer’s bank once there is a firm commitment to pay on a fixed date. This means payment is not received immediately, but on a date agreed between the parties.

Since this payment method is relatively balanced, it does not expose either party to too much risk. The seller only lets go of ownership and possession of the goods once payment or a firm commitment to pay is received. The buyer only pays when they see the documents for the goods, or even after taking physical delivery. This method also involves less cost overall than letter of credit, and it can be set up in less time.

However, just like letter of credit, the focus of both banks is on documents, and not necessarily the goods themselves. This means it may be harder to discover a problem with the quality of the goods before payment is made. The payment method also provides very little recourse for the exporter in the event that the importer fails to pay for the goods. Apart from these, documentary collections present a balanced payment method for both exporter and importer.

4. Open account (O/A)

This payment term involves a trade deal where the exporter agrees to deliver the goods to the importer without receiving payment until a later date. Payment usually falls due after an agreed period, typically 30, 60, or 90 days after delivery. Therefore, the importer essentially receives the goods on credit, with payment to follow at a later date.

Clearly, this payment method favors the importer, since they enjoy the position of taking delivery of the goods without making payment. It can have the effect of reducing their operating expenses, seeing as they can simply order the goods and try to sell completely before they have to pay the exporter. It also reduces their need for working capital, as they don’t have to worry about freeing up funds to complete payment before taking delivery of the goods.

Due to these advantages, importers are always keen to find exporters that provide open account payment terms. In a buyers’ market (one where there are more goods and less demand), you may see open account terms being the dominant mode of payment. Exporters that also want to display trust in a valued customer or that want to attract a valuable account may be more willing to offer these terms.

However, you should keep in mind that open account is also very risky for exporters. The risks of non-payment, late payment, bankruptcy, and other unexpected events are very high in this transaction. In addition, exporters essentially have to produce the goods and ship them without receiving payment. This can leave them with less working capital than they would like. Overall, this payment term has the potential to put exporters in a very delicate position.

For these reasons, it is very common to see exporters try to protect their position by exploring trade finance options. These are essentially mechanisms that help the exporter protect themselves against loss, pending when they receive full payment from the importer. Popular options exporters can explore include export credit insurance4 and factoring5.

You should only explore this option in situations where you have a low-risk trading relationship with the importer. Another possibility is where there is very low demand or where you are looking to win important customers.

5. Consignment

The final major payment term you should know about is consignment. Here, the exporter produces, ships, and delivers the goods to the buyer but only collects payment after the goods have been sold. You can often see this payment term being used by exporters who have distributors or third-party agents in foreign countries. Perhaps it may be rarer to find this situation in normal seller-buyer relationships.

The rarity of this payment term is based on a simple reason – the incredible risk it poses to exporters. The exporter bears all of the costs of producing, shipping, and delivering the goods to the importer. In addition, while the goods are in possession of the importer, they typically continue to be the property of the exporter. This means where there is an event like fire, theft, storm, or other damage, it is the exporter that bears the loss.

The exporter also bears the risk of non-payment or late payment by the importer. This is in addition to the risk that the goods may not even sell as well as the parties had hoped. As a result, exporters are understandably reluctant to offer or accept these terms from buyers.

The payment term is most applicable where there is an existing relationship between the exporter and importer. The importer needs to be reputable and trustworthy, and the goods must have been shipped to a country that is politically and commercially secure. In addition, this payment term simply cannot be accomplished without putting in place proper insurance measures and taking advantage of trade financing options6 where available.

Where the exporter is able to protect themselves well, consignment can also deliver advantages for them. It can be a good opportunity for exporters to enter new markets, reduce the costs of maintaining inventory (thereby allowing for lower prices), or simply make goods available much faster (leading to competitive advantages).

Other financial terms you should know about

Apart from the major payment terms, there are a few other terms that have evolved over the years. Here are a couple of terms you should know about:

- Bank payment obligation: This is one of the newer payment terms being offered in modern times. The process involves two banks – an obligor bank that acts on behalf of the importer, and a recipient bank acting on behalf of the exporter. The obligor bank signs an irrevocable undertaking to pay the price of the goods to the recipient bank on an agreed date. The payment is made once there is a successful matching of electronic data relating to the trade deal.

- Confirmed letter of credit: This is essentially a letter of credit, but with an important difference. Here, the letter of credit issued by the importer’s bank is confirmed by another bank of the exporter’s choice. The confirmation is more than just checking to see if the importer’s bank is solvent and capable of paying. The exporter’s bank also agrees to pay the exporter if the importer’s bank fails to pay.

How do the payment terms compare?

Now, let’s look at how the payment terms compare to one another in terms of the risk involved, and the pros and cons of each payment term. Here’s a table that shows the risk level of each term for exporter and importer.

The pros and cons of each payment term affect the exporter and importer differently. Here’s how these pros and cons stack up.

Cash in advance

For Exporter/Seller

✅Pros: Allows exporter collect most or all of the payment before shipment; Provides favorable cash flow.

❌Cons: No real disadvantage

For Importer/Buyer

✅Pros: Increases trust with the seller, especially where goods are really scarce.

❌Cons: Poses the highest risk due to possibility of non-delivery or delivery of low-quality goods; Potentially unfavorable cash flow situation, especially if the purchase was financed.

Letter of Credit

For Exporter/Seller

✅Pros: Applicable in many countries; Guarantee of payment backed by a bank

❌Cons: Potentially no recourse in the event of non-payment by the bank

For Importer/Buyer

✅Pros: No payment until delivery and inspection of documents.

❌Cons: Does not include inspection of the goods for quality; Quite expensive to set up. The process is also difficult to set up.

Documentary collections

For Exporter/Seller

✅Pros: Only lets go of goods upon payment or receipt of firm commitment to pay; Relatively little risk exposure since ownership and possession is not transferred until payment.

❌Cons: DA terms can mean payment does not come, even after delivery; Risk exists that the buyer will fail to pay on a fixed date for DA terms; Potentially no recourse if buyer fails to pay since the transaction is not guaranteed by a bank.

For Importer/Buyer

✅Pros: Only pays for goods upon inspection of documents for regularity; Potentially allows delivery and possession of goods before payment, especially for DA terms.

❌Cons: Does not include inspection for quality of goods delivered.

Open account

For Exporter/Seller

✅Pros: Very lucrative term to attract importers in buyers’ market.

❌Cons: Risk of non-payment or late payment which will potentially stretch exporter’s working capital; Must factor in the extra cost of securing insurance, or utilizing trade finance options.

For Importer/Buyer

✅Pros: Allows possession and potential sale of goods before payment; May enable flexibility in working capital since no immediate need to pay for goods; May sell goods and recoup profits before paying for goods, depending on the credit period; Potentially lowers operating expenses.

❌Cons: No real disadvantage

Consignment

For Exporter/Seller

✅Pros: Potentially helps supply goods quicker, leading to competition gains; Enables ready access to new markets; Eliminates the cost of holding inventory, potentially allowing space to offer a more competitive price.

❌Cons: Bears all the costs of production, shipping, and delivery to the importer; May not recoup costs if goods do not sell as expected; Continues to retain ownership of goods, even after delivery, and will bear the cost of loss, theft, or damage.

For Importer/Buyer

✅Pros: Eliminates the cost of procuring goods, thereby minimizing operating costs; Does not bear the risk of the goods since ownership does not pass.

❌Cons: If goods do not sell, will have taken a loss on the costs of inventory.

How to pick between payment terms?

The delicate balancing act required when deciding on payment terms means it’s unlikely to be an easy task. As you make your decision on what terms to offer, the following tips will be helpful:

- Consider your financial needs and strengths.

- Think about your negotiating position. If you are in a stronger position, you may be able to demand more favorable terms.

- Does the other party come from a country with significant commercial or political risk? You may want a more secure term here.

- In certain industries, specific terms are generally used. For instance, in the food and textile industry, it’s common to see documentary collections being used, while letters of credit are common in oil and gas.

- Prevailing market conditions can be important. If it’s a sellers’ market, you may be able to set the most favorable terms for yourself as an exporter.

Overall, it is important to keep in mind that you don’t have to pick just one of these terms for your entire transaction. A mix of terms can apply at different stages, such as before production, before shipment, and upon delivery. Consider how a mix of these terms can provide a more balanced transaction for you.

Final thoughts

Deciding on payment terms is an important part of international trade. Although the process of setting these terms can be difficult, the positive trade-off is you are able to minimize the risks of the trade – which is always a good thing.

Want to know more about how Alibaba.com can help you trade globally and expand your business? Speak to an expert now.

Further reading on international trading:

- How to sell and export goods to the US

- 12 import-export business ideas to start in India

- How to start exporting: the ultimate guide

- What are trade terms: Incoterms explained (DDP, FOB, EXW, FCA)

References:

1. https://www.tradefinanceglobal.com/trade-finance/payment-methods/

2. https://www.investopedia.com/terms/l/letterofcredit.asp

3. https://www.thebalance.com/what-is-escrow-315826

4. https://www.trade.gov/export-credit-insurance

5. https://www.entrepreneur.com/encyclopedia/factoring

6. https://www.gtreview.com/what-is-trade-finance/

Start your borderless business here

Tell us about your business and stay connected.

Related Reading

Keep up with the latest from Alibaba.com?

Subscribe to us, get free e-commerce tips, inspiration, and resources delivered directly to your inbox.